College alumni and the parents of college students have grown quite accustomed to the persistent phone calls and snail-mail pleas for donations. It’s not like the robo-call you just hang up on, or the junk mail you trash. Colleges have a place in the heart. Their base wants to help.

The University of Cincinnati is right up there in turning former students into donors. Its endowment of nearly $1.2 billion ranked 74th in the United States and Canada last year, third in Ohio. “From creating vital student scholarships to funding leading-edge research to providing for world-class patient care, our donors make a difference,” the UC Foundation says on its website.

But what does UC and its foundation do with the money before spending it? About a fourth of it sits in restricted trust accounts set up by donors. Another chunk goes into real estate projects. The rest, $784 million as of last June 30, is invested.

Karl Scheer (Photo by Hailey Bollinger)

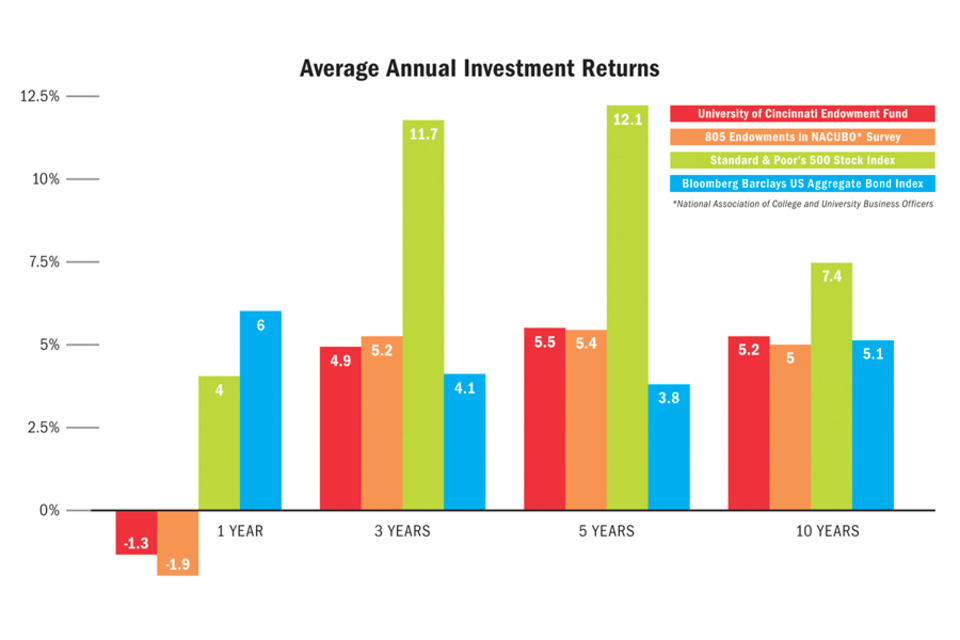

Not that well, it turns out. Even though the markets for U.S. stocks and bonds generated returns of 4 and 6 percent, respectively, in the collegiate fiscal year that ended last June 30, UC’s investment portfolio lost 1.3 percent. In monetary terms, $8.3 million went down a hole somewhere.

How did UC manage to lose money in a rising market?

To be sure, most college endowments did. The 805 U.S. university endowments responding to the annual National Association of College and University Business Officers survey lost an average of 1.9 percent of their money in the 2015-16 school year. Where did they go wrong?

Their skittishness after the 2008-09 stock market crash sent them into ever-larger plays on so-called “alternative” investments. That sector includes real estate, but also a controversial species of investment known as hedge funds. Nearly $1 of every $5 in UC’s $784 million portfolio is in these things.

No one is suggesting that UC put all its eggs in one basket, but some of its edgier baskets have cost donors millions in losses and missed opportunities.

Its hedge fund basket, worth $144 million as of last June 30, returned an average of 2.7 percent over each of the last five years. Meanwhile the S&P 500 index returned 12.1 percent a year.

Apply those returns to a hypothetical stash of $125 million, and the difference is $78.5 million, according to a calculation by Schaeffer’s Investment Research in Blue Ash. How many scholarships could UC have funded with $78.5 million?

A 54 percent drop in the U.S. stock market between 2007 and 2009 sent UC down the hedge fund path. Karl Scheer, who became UC’s chief investment officer in 2011, says hedge funds diversify the portfolio’s exposure to risk. Still, he says, the UC Board of Trustees’ Investment Committee in April lowered its hedge fund allocation from 20 to 18 percent.

“Part of the reason hedge funds have done so poorly is that market forces have favored things like U.S. equities (stocks),” Scheer says. “We would expect them to do well at different times. If U.S. equities start to do poorly, we would expect these to do relatively much better. We believe we’re pretty well positioned for a (stock market) correction. If one should happen tomorrow, we would expect to outperform benchmarks by a lot.”

That broadened exposure comes at a high cost. While hedge funds make up 18 percent of UC’s investments, they accounted for 38 percent of the fees paid to its outside money managers in 2015-16. Ever since UC dipped into hedge funds, those funds have cost big money — $2.3 million in fees last year alone — for low returns.

“Alternatives fees are sometimes three to 10 times larger than regular investments,” says Chris Tobe, vice president of investments at First Bankers Trust in Louisville and a former trustee of the Kentucky public employees retirement plan. “They’re paying excessive fees for strategies that have not provided the values that were expected.”

The UC endowment’s strategy of diversifying away from stocks and bonds has deprived it of sizable returns in periods that ended June 30, 2016.

Graphic by Dylan Robinson

UC’s hedge funds are not household names like Apple or Procter & Gamble. It has $27 million in its biggest hedge play, a brew of distressed and restructuring companies run by King Street Capital Management in New York. That fund netted exactly nothing in 2015-16. UC lost $1.7 million of its $14 million stake in the Claren Road Credit Master Fund and $600,000 of its $10 million position in the Centerbridge Credit Partners Offshore Fund.

Scheer said the UC investment committee dumped Claren Road at the end of last year. It stuck with Centerbridge, which is now running well in the black.

What is in these funds? CityBeat sent UC a public records request for a breakdown of their holdings.

Three months later UC’s general counsel’s office declared them to be trade secrets exempt from the Ohio Public Records Act. Ohio State University says the contents of its $648 million in hedge funds are trade secrets, too. Unlike UC, OSU refuses to disclose how well, or poorly, its hedge funds performed. Its entire portfolio, 18 percent of which is in hedge funds, lost $128 million, or 3.4 percent.

So when you donate $10,000 (or $10) to UC or the UC Foundation, you won’t know if your money went into a stock, a bond, an IOU from a fading restaurant chain, or a Peruvian goat farm. If a UC trustee wants to know the underlying holdings of a hedge fund, Scheer says, he or she would have to accompany UC investment office staff to the fund itself, most likely in New York, to get a glimpse.

“We asked our fund managers what we’d be able to share,” he says, “and the overwhelming response back to us was, if you share the contents of our portfolio, you will put our companies at a potential disadvantage.”

Sounds like what Bernie Madoff might have told a nosy accountholder before his corrupt fund — the biggest Ponzi scheme ever — imploded in 2008. It is quite possible that UC donors aren’t insisting on more transparency because they don’t know that the fund contents are secret.

As a general rule, transparency is important in investing, says Joe Bell, senior market strategist at Schaeffer’s Investment Research.

“It’s important that you have the ability to know exactly where your money’s being invested,” he says. “They shouldn’t be shielding the investments from donors.”

Tobe agrees. He knows that hedge funds dabble in esoterica like offshore limited partnerships, collateralized securities and private debt. Moreover, he says, they go in and out of things.

“The lack of transparency is troubling,” Tobe says. “You don’t even know what country your money’s in. You don’t know where it is.”

Scheer, who is very forthcoming in person, describes UC’s hedge fund holdings as opportunistic and mostly in the U.S. Its funds buy distressed debt, such as Puerto Rican bonds. They look for openings to make money on valuation spreads in corporate mergers and other situations.

“If you’re buying a company’s debt at 20 or 30 cents on the dollar and you think it’s worth 80, that can be very profitable and not that risky,” Scheer says. “When it’s a fire sale, you can buy some very attractive assets at a huge discount to their actual value.”

Scheer says his office expected average annual returns of 6 to 8 percent on hedge funds. He still hopes to get there. But the wait, he says, has been frustrating.

“If we thought they were going to continue to generate returns like this, we would greatly reduce our allocation to (hedge funds),” he says. “Unfortunately, we’ve got to look forward and see what’s going to happen next.”

James McNair is a reporter for City Beat. Reach him at jmcnair@citybeat.com, 513-914-2736 or @jmacnews on Twitter. This story first appeared at City Beat and has been used by permissionl