Home lending in major counties in the Cleveland Fed’s region was strongly impacted by the Great Recession, say Fed researchers.

Nearly 10 years into the economic recovery, home mortgage lending in the Fourth Federal Reserve District (Ohio, western Pennsylvania, eastern Kentucky, and the northern panhandle of West Virginia) remains affected by the Great Recession, according to a series of analyses of Home Mortgage Disclosure Act (HMDA) data by Federal Reserve Bank of Cleveland researchers Lisa Nelson and Matt Klesta.

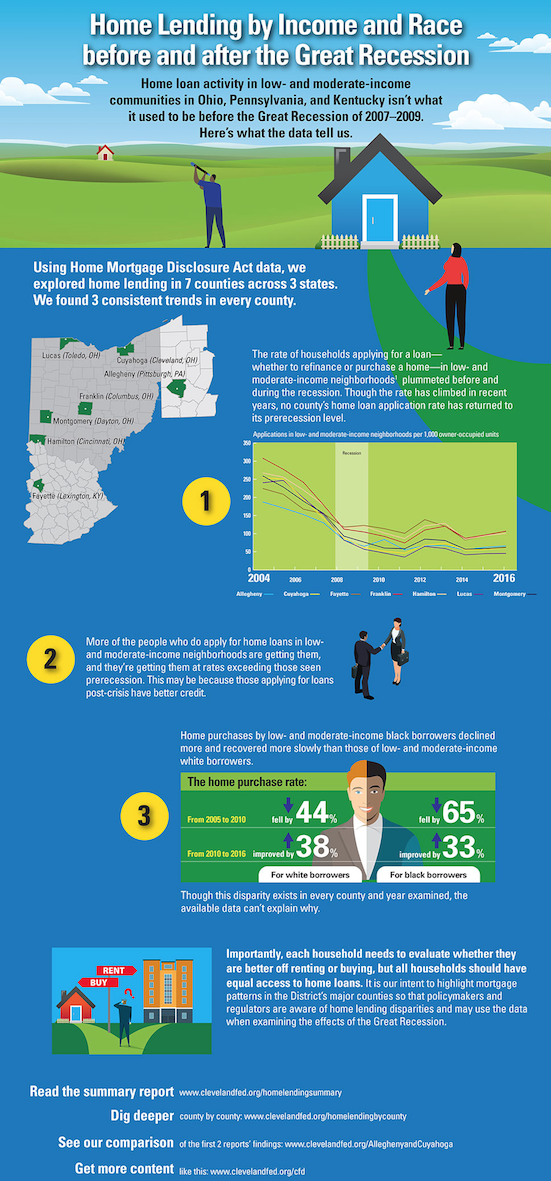

Nelson and Klesta examined home lending conditions within and across seven major counties in the Cleveland Fed’s region—Allegheny, Pennsylvania (Pittsburgh); Cuyahoga, Ohio (Cleveland); Fayette, Kentucky (Lexington); Franklin, Ohio (Columbus); Hamilton, Ohio (Cincinnati); Lucas, Ohio (Toledo); and Montgomery, Ohio (Dayton). Focusing on the economic recovery in low- and moderate-income (LMI) neighborhoods and among white borrowers and black borrowers, the researchers found that:

• Home mortgage loan application rates in LMI neighborhoods in the seven counties plummeted as the Great Recession took hold, and they remain well below prerecession application rates. However, the rate of loans moving from application to origination in LMI neighborhoods has broadly increased since the recession and now exceeds pre-recession rates.

• In every county examined, black borrowers experienced larger declines in home purchase rates than did white borrowers from 2005 to 2010. While home purchase rates increased from 2010 to 2016 for both races, the gains were lower among black borrowers when compared to their white counterparts. The researchers note that the race disparity persists regardless of borrower income.

According to Nelson, coauthor (with Logan Herman) of a report that summarizes the researchers’ findings, “It is important to note the data used in these analyses do not include all of the factors lenders use to determine the creditworthiness of the borrower.

Also, each household must evaluate whether it is better off renting or buying.” Nelson says she and Klesta are highlighting mortgage patterns in the region’s major counties so that policymakers and regulators are aware of home lending disparities and may use the data when examining the effects of the Great Recession.

Read An Uneven Recovery: Home Lending in the Fourth District by Race and Income.

Read the latest Metro Mixes, snapshots of local economic conditions.

Visit the website at clevelandfed.org.

The Cleveland Federal Reserve